The Retirement Planning : Is Your Social Security Taxed?

Retirement is the longest unemployment period. For funding retirement years, many of us plan for 401k withdrawals and Social Security. But we miss to factor in the taxes. Do you know, up-to 85% of your Social Security money can be taxed? When 85% of social security money is taxed, the overall retirement funds can runout 5 to 7 years quicker than the plan. In this article, we will discuss the calculations that determines how much percentage of your social security is taxed.

Let's discuss the following topics to understand more.

- Provisional income and how it's calculated.

- How Provisional income determines Social Security Tax.

- Two different retirement scenarios.

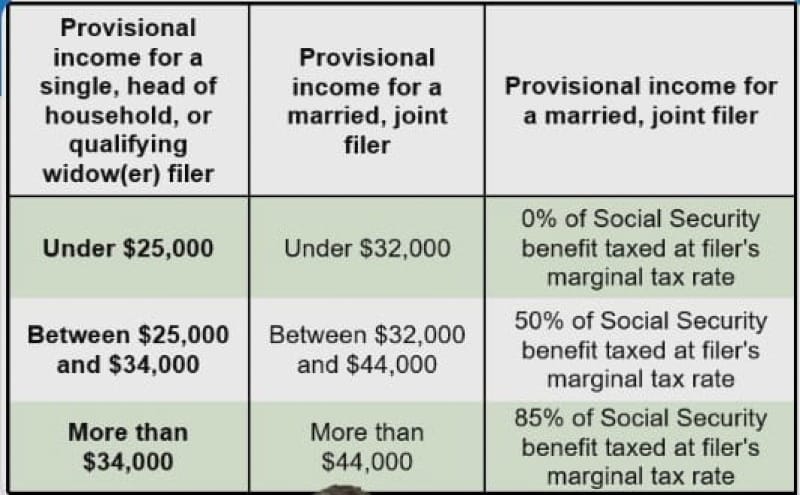

Provisional income and how it's calculated

Provisional income is a term used primarily in the context of U.S. federal taxes to determine how much of your Social Security benefits are taxable. Below are the steps to calculate your provisional income.

-

Start with your Adjusted Gross Income (AGI): This includes

wages from any parttime job, 401K withdrawals, dividends, interest,

rental income, capital gains and other income. -

Add nontaxable Interest: This could be from municipal bonds or other

investments that are exempt from federal income tax. Yes! Though this

is tax free interest, it gets added in provisional tax calculation. -

Add Half of Your Social Security benefits.

The total sum of these components gives your provisional income.

How Provisional income determines Social Security Tax

Let's look at the relation between provisional income and how the social security money is taxed.

So, for married joint filers, if the provisional income is more than $44k, then, 85% of Social Security is taxed.

Two different retirement scenarios

Let's take an example of a family of 4. Husband, wife and 2 kids ages 8 and 10. Their current expenditure is $100k per year. It includes their mortgage, vacation, and all other daily and monthly expenditure. When the husband and wife retire in 15 to 20 years from now, they will not have expenditure for kid's activities, mortgage .. etc. But considering inflation, assume they need the same $100k to live comfortably during retirement. This includes medical expenditure as well.

Let's see what happens if they plan their retirement funds like below.

Scenario 1

$40k - 401k Withdrawals.

$5k - income from municipal bonds.

$20k - Social Security(SS) money.

$35k - Rental income, Dividend from stocks, mutual funds ... etc.

Provisional income is $40k + $5k + $10k (50% of SS money) + $35 i.e., $90k.

Because provisional income is more than the threshold(44k), up-to 85% of their social security will be taxed.

Scenario 2

The same family funds their retirement money of $100k like below.

$10k - 401k withdrawals.

$5k - income from municipal bonds.

$20k - Social Security money.

$5k - Dividends from stocks and bonds.

$20k - HSA account to take care of all medical expenditure.

$20k - ROTH IRA.

$20k - Cash value life insurance(CVLI) .

Your HSA when used for medical expenditure won't be taxed. ROTH IRA and CVLI are built with post tax money. So, there is no tax while withdrawal. It doesn't even factor into provisional income and taxable income calculation.

So, the provisional income is $10k + $5k + $10k (50% of SS money) + $5k i.e. $30k.

Because provisional income is less than $32k, Social security money is not taxed.

Conclusion

In our example scenarios, the family is funding the same $100k. But based on how they fund, they can control how much of their social security is taxed. Also notice that in Scenario1, not only the provisional income is high, but their overall taxable income is also going to be high. But let's leave that calculation for another day. Planning your retirement as Scenario2, can't happen in few days or even few months. It's a multi-year project. The sooner you start the more tax efficient your retirement is going to be.

That's a wrap for this week. Happy learning!