The Fragile Decade of Your Retirement

There are banks that provide loans for home purchases and children's college education, but I haven’t found any bank that offers loans for retirement. In retirement, we need a fixed monthly income generated by the assets we've built over our lifetime. More importantly, we need the certainty that this income will continue, no matter what happens in the world. In this article, we will discuss one critical risk in retirement planning and how to manage it.

- Sequence-of-returns risk

- Let the numbers speak

- Strategy to handle this risk

Sequence-of-returns risk

Most of our retirement accounts like 401k and IRAs are invested in market and 100% subjected to market risks. Sequence-of-returns is a risk we face in later point of our life around retirement due to negative market conditions. This risk is significant few years before the retirement and few years after the retirement. Let's call it as fragile decade of our retirement. In the retirement, withdrawing money from these accounts already effected by negative market will deplete these accounts many years earlier than anticipated.

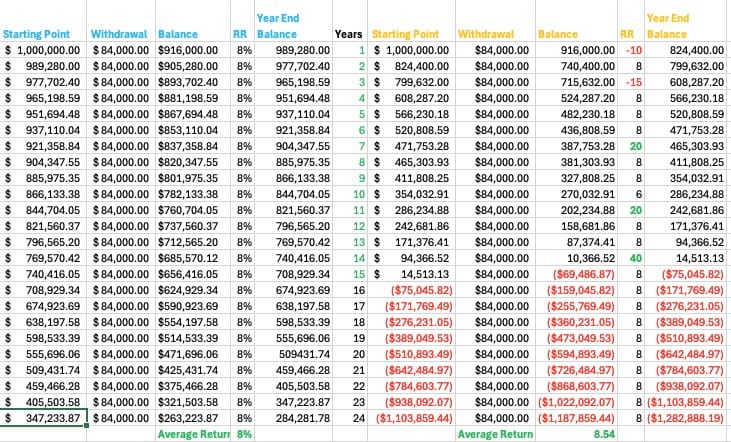

Let the numbers speak

Let's look the retirement account of Mr. Peter retiring at age 60 with $1M. Peter is expecting the account will last 25 to 30 years which is the typical retirement duration. The first 5 columns with headers in blue gives the projection when the money giving 8% rate of returns (RR) consistently in the market.

The last 5 columns with headers in yellow, works with the same $1M but gives the projections when the market has done -10% and -15% in the first and 3rd year respectively. Is this a practical example? Can the stock market do -10% and -15%?

Let's look at the first 5 columns again. Peter is withdrawing $84k from the account every year to support his retirement. The account lasted 24 years and still $263k balance left. So, this account will serve the typical 25 to 30 years of retirement.

But in the last 5 column, when hit by market negative cycles in the 1st and 3rd year, the account depletes in 14 years. Though there are very good returns in

Year 7, Year 11, Year 14 with 20%,20%,40% gains, the account didn't last more than 14 years. This illustrates how the sequence of returns can greatly impact the retirement accounts. The negative market cycles few years before and few years into the retirement can have significant effect on how long the account will serve.

Strategy to handle the risk

It's good idea to start moving some part of the retirement assets into investment vehicle that are protected from market risk. Products based on indexed contracts is a good way to do this. It helps us to have the security against market volatility, but at the same time take decent gains when the stock market does good. I have written few short articles previously on Fixed Indexed Annuities and Indexed Universal Life products. From the home page of my website, you can use the right top search icon and search with keywords Fixed Indexed Annuities and Indexed Universal Life to find the corresponding articles. Both products help with creating a safe and sound retirement strategy.

That's a wrap this week. Happy Learning!

Please post your questions in the comments section of this article. I will answer every question.