Navigating the World of Annuities in the USA

What is an Annuity?

Annuity is a contract with the life insurance company that provides certain benefits in exchange for a deposit of money, known as premium. One of the main uses of annuities is to provide income during retirement. In this aspect, we can compare annuities with our social security. While social security is a government pension program, annuities can be used as a private pension plan. When it comes to social security, we have very limited control over the benefits and government can decide to increase/decrease benefits based on various other factors. With annuities, we have control on how we want to configure our annuity and choose from different options provided by the insurance companies.

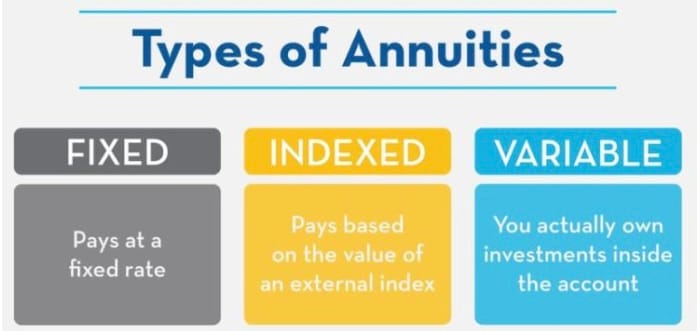

There are mainly 3 types of annuities.

Variable annuities are like investing in stocks and mutual funds. When we are talking about money generating pension plan, we don't want to expose that money to market by putting them in stocks and mutual funds. I am sure most of us have enough stocks and mutual funds already exposed to the market and we don't need another vehicle doing the same . So, I don't recommend going for a variable annuity and will not talk about it further in this article.

With that, we are left with only 2 types i.e., Fixed Annuity and Fixed Indexed Annuity.

Fixed Annuity

Provides a guaranteed interest rate and steady income stream, offering a secure way to grow savings with low risk.

Fixed Indexed annuity

Links earnings to a stock market index, offering potential for higher returns with a guaranteed minimum. We get best of both worlds by combining growth opportunities with protection. The funds are not directly invested in the market, but the returns credited to our account are linked to how stock market indexes perform. There will be ceiling and floor as well. Normally the floor is 0% and ceiling varies based on company and product. Let's take the ceiling as 8%. If stock market gives 15% returns in a year, we will be credited only 8%. But if the stock market goes negative by 15% next year, we will not take the loss as the floor is 0%.

Only 2 types! of Annuities. That's so simple!

Sorry to disappoint you :-) We got to go one more level deeper now.

Based on the lifecycle of the annuity, they are further divided into 2 categories. Before we talk about those, we need to understand the lifecycle of an annuity.

The annuity has 3 phases.

- Contribution

- Accumulation

- Annuitization

Contribution

This is the duration we contribute to the annuity. We can contribute to annuity over the time with monthly/annual premium or we can pay single premium and be done with contribution phase.

Accumulation

This is the phase we will let our money grow with the investments done by insurance company. Insurance company invests the money in different sources to make sure they give us returns illustrated during the contract.

Annuitization

This is the duration where we use the annuity as a private pension plan and withdraw the money. Again, you can choose to withdraw all the money at one shot or over the years. It's a private pension plan. So, it must have more flexibility than government provided social security plan. Isn't it?

Now that we know the 3 phases in the lifecycle of an annuity, let's discuss the flexibility we have around these phases. If you let your annuity, go through all the 3 phases, it's called Deferred Annuity. If you want to eliminate the Accumulation phase and directly move from Contribution phase to Annuitization phase, it's called Immediate Annuity.

So, based on the returns you expect from annuity, there are two types i.e., fixed and indexed. Based on whether you want your annuity to go through all phases or cut down one phase, you have two types i.e., Immediate and Deferred. Now, tell me how many total annuity types we can come up with?

You are right. It's 4 (2 x 2). Here they are.

- Fixed Immediate Annuity

- Fixed Deferred Annuity

- Immediate Indexed Annuity

- Deferred Indexed Annuity

Fixed Immediate Annuity

We contribute to the annuity and expect a fixed rate of return. This is like bank savings account. In this Annuity, we are not giving time for accumulation and starting to withdraw immediately(next month/year) after the contribution. Fixed Immediate annuities require a lump-sum premium.

Fixed Deferred Annuity

We contribute to the annuity and expect a fixed rate of return. This is also like bank savings account. But we are giving time for our contributions to grow and annuitization starts sometime in future. The amount we can withdraw during annuitization will be more when compared to immediate annuity because we are giving time for the money to grow.

Immediate Indexed Annuity

Here the returns are based on stock market indexes. Though the insurance company doesn't invest all your money into market, it uses the index performance to decide how much returns to give you on your annuity. Here also we are cutting down the accumulation phase and starting to withdraw immediately(next month/year). Immediate indexed annuities, like other immediate annuities, typically require a lump-sum premium.

Deferred Indexed Annuity

Here also the returns are based on stock market indexes. You do let the annuity go through accumulation phase and grow the money. The amount you can withdraw during annuitization phase will be more compared to Immediate Indexed annuity.

That's a wrap this week. Happy learning!!

We will continue to discuss more related to annuities in coming weeks.