Navigating the Life Insurance World in the USA : Building Wealth with CVLI

Life insurance is the concept of transferring the financial risk a family can't afford to a big company that has the resources and funds to handle. Imagine 100 families pooling the money with one big insurance company. The insurance company safely grows the money and in case of unexpected things happen to any family the company will give the money to the family as death benefit. Only lower single digit percentage of the families will go through unexpected things like a family member passing away early in life. While these families are given the death benefit, 95+ families will get the peace of mind and sense of security for the premium they are paying.

While insuring life is one aspect, life insurance companies have come up with different types of life insurances to build cash value. Since then, it has become a tool for smart investors, rich people, and organizations to grow money in tax efficient manor in cash value life insurance(CVLI). Life insurance proceeding are the perfect way to pass wealth to next generation in tax efficient manner.

The premium for 1M dollars coverage for 30-year-old in great health can vary from tens of dollars to hundreds of dollars per month based on the type of the product.

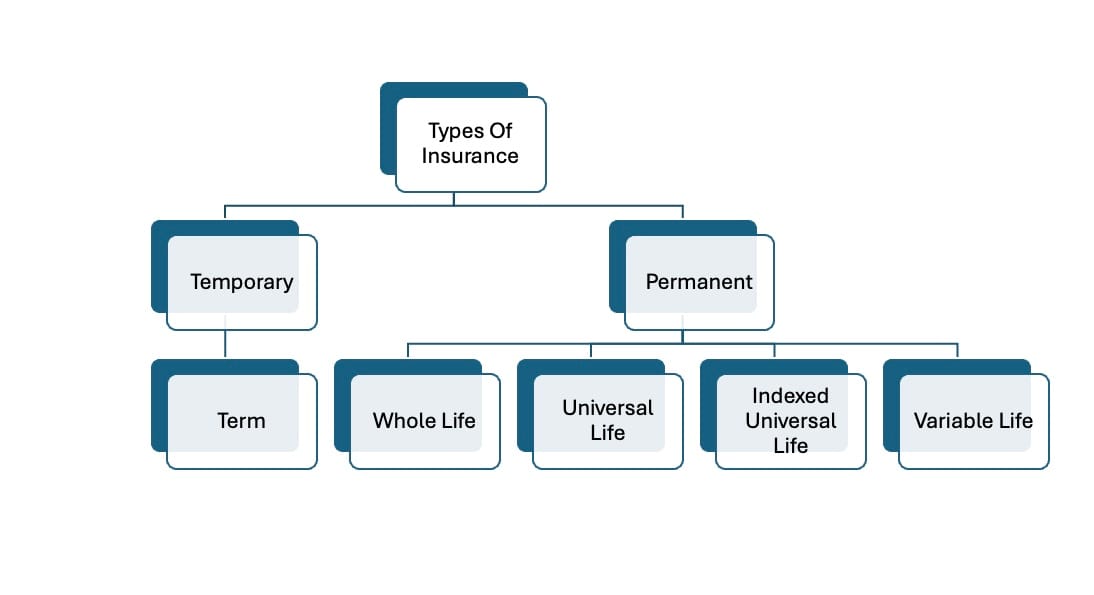

First let's see the types of life insurances available and then discuss the characteristics of each.

Temporary - Term Life Insurance

As the name suggests, it covers someone's life for fixed term. Normally these policies are available for 10, 20 and 30 years. Some companies offer 35 years too. These are purely death benefit purpose. Best for temporary financial protection, like paying off a mortgage or providing for children until they become financially independent. The premiums for term policies are lower and fixed during the term.

The premium for 30-year-old in great health, 20 years term and 1M coverage will be around $30 to $50 per month. There is no cash value in term insurance.

Permanent-Whole life

What if someone want to use the insurance product as an investment vehicle also and use the money while they are alive?

What if someone want to use the insurance product as a vehicle for transferring wealth to next generation (legacy transfer)?

Permanent lie insurance is born to address these needs. The proceedings from the insurance products are tax free. Hence the permanent life insurance became a smart investor choice and became popular as cash value life insurance (CVLI). The wealthy people use CVLI to its best to fund their businesses and transfer millions of dollars to their next generation.

For whole life, the coverage will be lifelong. That means the insurance company must pay the death benefit at some point in time. Hence the premiums will be higher. Also, there is cash value and it grows at a guaranteed rate. This guaranteed rate is normally between 2 to 3%.

The premium for 30-year-old with great health, for 1M coverage can cost around $500 - $700 per month. After 20 years, the cash value accumulation will be around $150k to $200k.

Permanent - Universal Life

This is like whole life, but the premiums can be adjusted with in certain limits. Death benefit also can be adjusted over time. The cash value grows at the current interest rate. So, the interest rate can change based on the interest rates in the bond market, inflation, and economic growth trends.

The premium for 30-year-old with great health, for 1M coverage can cost around $600 - $800 per month. After 20 years the cash value accumulation will be around $150k to $250k.

Permanent- Index Universal Life(IUL)

Things get more interesting here. In index universal life, the returns are based on the market indexes like S&P 500 and fidelity indexes. Though the insurance company doesn't invest all the money directly in stock market, the returns given in the product are calculated based on how the indexes do. The insurance company gives set of indexes to choose from. There will be caps and floors on the interest rates. For example, if the cap rate is 10% for S&P 500 index in this product and the S&P 500 returns 20% in the market, the interest rate credited will be only 10%. At the same time, there is generally a 0% floor. If he S&P 500 index returns -20%, the interest rate will be 0%. You will not lose any cash value due to market performance. So, moderate growth with no downside risk.

The premium for 30-years-old with great health, for 1M coverage with 20 years pay can cost around $1200 - $1400 per month. After 20 years the cash value accumulation will be around $400k to $500k.

Permanent - Variable Life

Here the cash vale varies along with the stock market as the money will be invested directly in the market. So, the money is exposed to all the positives and negatives in the stock market.

The premium for 30-years-old with great health, for 1M coverage can cost around $500 - $700 per month. After 20 years the cash value accumulation will be around $0k to $350k.

That's a wrap this week. Happy Learning!